Comparing contents insurance (sometimes known as renters insurance) regularly is a smart move for both renters and home owners in New Zealand. Like any shopping you do, comparing often saves you money and gets you more for less.

It's worth noting that insurance providers regularly update their contents insurance pricing and offerings, meaning the best contents policy for you last year might not be the best for you this year.

Read on to learn more about why you should compare contents insurance, how to compare contents insurance and how much you could save by comparing your contents insurance.

Quashed makes comparing multiple contents insurance quotes and policy benefits quick and easy, ensuring you’re not missing out on better policy coverage or significant savings.

Three reasons why you should compare your contents insurance

First, you could save a significant amount of money.

We’re talking potentially hundreds of dollars each year – simply by shopping around. Insurance premiums can vary a lot between providers and many Kiwis are unknowingly paying more than they have to by just sticking with their current insurer.

Second, beyond the obvious money savings, comparing your contents insurance helps you to find policies better suited to your needs. Contents insurance policies are not all the same.

When it comes to insurance policies, they are not all the same, even though most of us think they are.

At claim time, the differences between policies can have a big financial impact on you. For example, one insurer may offer you a standard cover of up to $3,000 on your jewellery, whereas another may have a standard policy for up to $10,000. One may offer $20,000 in temporary accommodation cover in the event your property is not livable (e.g. after a fire or flood), and another insurer may offer you up to $40,000. Not all policies are the same when you look at them closely.

Third, insurance companies are constantly changing their pricing and policy benefits.

A contents insurer offering you the best price and benefits last year could well be one of the most expensive ones in the market this year. Insurance providers, including contents insurers, regularly update their pricing, offerings and introduce new features to stay competitive. What’s more, your own circumstances change over time – the policy that was perfect three years ago might not be the best fit now. You may have bought a lot more "stuff" since the last time you took out your policy and selected the sum insured amount or you could have gone and gotten rid of lots of things you own. Different sum insured amounts can change the cost of your policy significantly.

Now that we’ve covered the “why”, you’re probably thinking it’s still too much of a chore to compare my insurance… If you read no more of this article, read this – Quashed.co.nz makes it quick and easy to shop multiple quotes and compare policy benefits in less than 5 minutes. Find out how much you can save today.

How much does contents insurance premium cost in NZ

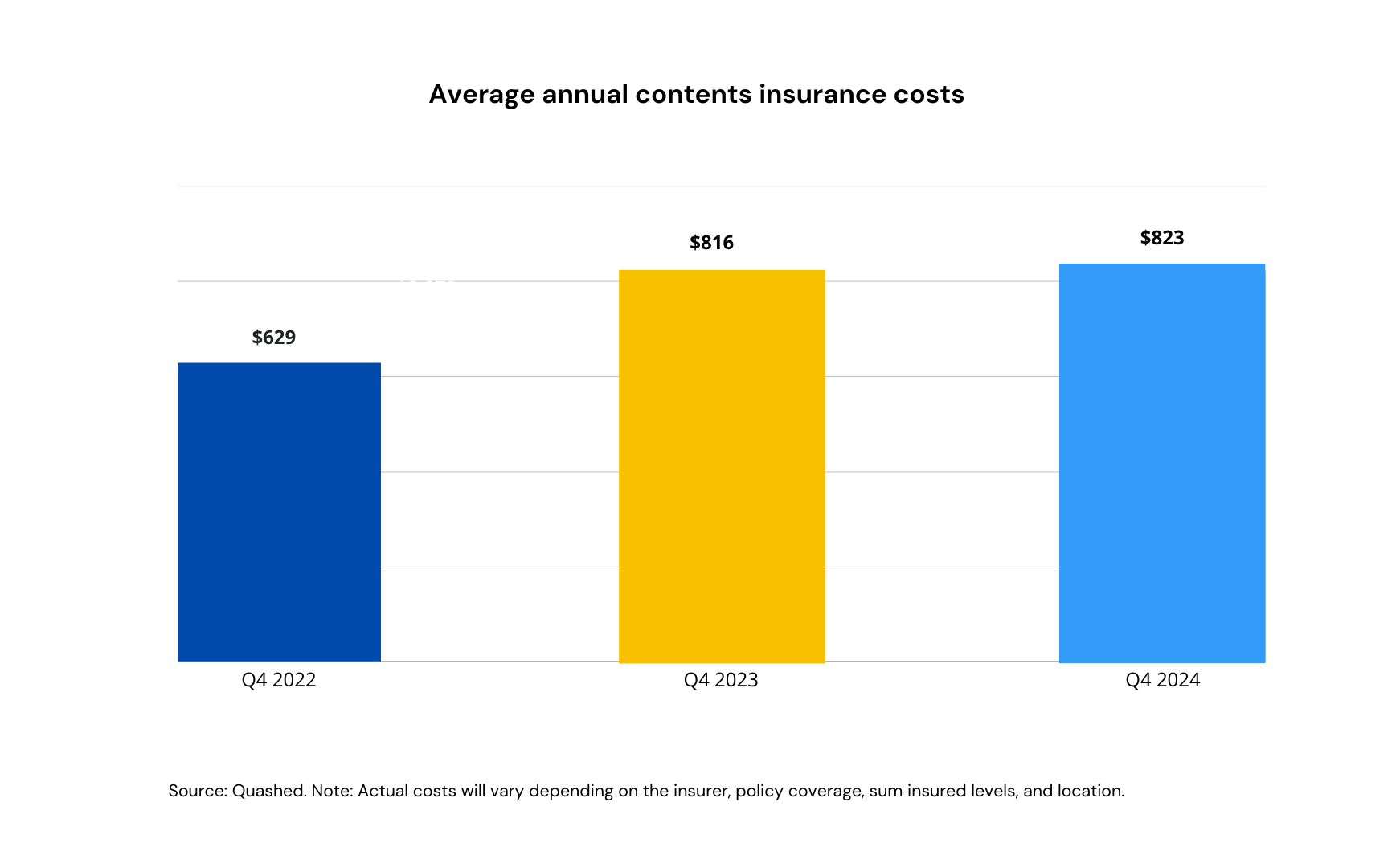

Contents insurance premiums is up 31% in New Zealand over the past three years (Q4 2022 to Q4 2024).

The average cost of contents insurance in NZ is now $823 a year (based on Q4 2024 Quashed data). This is up more than 30% compared to 2022 (Q4) when the average house insurance policy cost $629.

| Average house insurance premiums (yearly) |

2022 | $629 |

2023 | $816 |

2024 | $823 |

Depending on where you live in NZ, your house insurance premiums can be very different. Here’s a look at the key regions across NZ and how much average house insurance costs in Q4, 2024 data from Quashed.

Region | House insurance premiums (yearly) |

Auckland | $754 |

Canterbury | $891 |

Wellington | $990 |

Factors that impact the cost of contents insurance

The cost of contents insurance is impacted by a number of factors including:

Location of the property the contents is stored (natural hazards risk, theft risk, etc.)

Construction materials of the property (including quality of the build)

Condition of the property

Security features

Other selection factors that will change your premiums:

Coverage type (low or high tier of cover)

Sum insured amount

Excess

Add-ons selected

Payment frequency

Claims history

Now that you’re aware that the cost of contents insurance has risen significantly and there are a number of factors that impact on your premiums, let’s take a look at how you should compare your contents insurance to help you save money and find the best policy for you.

How to compare contents insurance in NZ

There are three areas you’d want to compare when it comes to your contents insurance.

Price (how much will it cost you)

Policy benefits (what can you claim on)

Insurance provider (who is providing your policy)

1. Price is the obvious one. We can only buy what we can afford. You may be surprised to learn that contents insurance premiums can vary a lot across insurance providers.

For example, contents that are insured for $100,000 with a $250 excess in Southland can cost between $580 to $981. This range is across four insurance providers. All other variables entered are the same when obtaining these quotes.

Tip: Contents insurance premiums can be significantly different across insurers. More expensive doesn’t mean you’re getting better cover. Cheaper contents insurance does not mean it is not as good.

2. Policy benefits are next on the list to look out for. Now that you’ve got an idea of a range of prices (commonly known as insurance premiums) across a number of insurance companies, you’d want to compare and understand how the policies are different. What can you claim on each policy and how the benefits and limits are different.

Now looking at the benefits of the policy i.e. what can you claim on. There are a number of cover benefits that are provided within a contents insurance policy. Temporary accommodation, liability for property damage and injury, mobile phones and laptop cover, jewellery, carpet, camera, artwork, locks and keys, are just some of them. Not all insurers will offer the same benefits nor the same limits.

Take bicycle cover as an example. If yours was stolen and it was worth $7,000, one insurer may offer $2,000 based on their standard cover and another may only offer $10,000. Assuming, you have not specified the bicycle for more on the policy and are relying on their standard cover limits. Another example, would be an insurer will cover temporary accommodation for up to $20,000 and another has $30,000 in cover limits. There could be a $10,000 difference at claim time with what comes out of your pocket.

When it comes time to claim, the difference in policy benefits could mean hundreds, or sometimes, thousands of dollars in difference.

Tip: The most commonly known insurance brands may not always have the most comprehensive policy benefits and limits.

3. Last, but certainly not least, the insurance provider behind your policy.

Most Kiwis will be familiar with three, maybe four, contents insurance brands in NZ. AA, AMI, State and Tower are the most commonly known brands. However, you may be surprised to know that there are more than 10 contents insurance providers/brands in the NZ market. AMP and Initio just to name a couple of alternative options. There are of course also the banks that offer contents insurance. ANZ, ASB, BNZ and Westpac to name the big fours.

But, does bigger brands always mean better insurance and lower prices?

Some of the lesser known brands offer sharp pricing, strong policy benefits and great service. And if you’re wondering, are they any riskier to insure with compared to the better known brand insurers? One way to look at it would be the financial ratings of the lesser known brand insurers. In New Zealand, all insurers are equally held to a similar standard by the Reserve Bank of New Zealand (RBNZ) and are subjected to the same regulations enforced by the Financial Markets Authority when operating in the country.

How much can you save comparing your insurance

With contents insurance climbing 31% in three years (Q4 2022 to Q4 2024), the short answer is you could potentially be saving a lot of money.

On average, based on data from Quashed.co.nz, a NZ consumer shopping for their contents insurance can expect to find that prices will vary between 20% to 100% across insurers. From Quashed’s 2024 data, we find that Kiwis could save $275 on average when it comes to contents insurance.

Based on this, a household over 10 years, assuming this holds constant, would be saving in excess of $2,500. This is on contents insurance alone, not including potential savings on car and house insurance.

Does that mean you’ll save the $275 on your house insurance today? It depends. You could save more, less or none at all. The best way to find out is to compare and shop for your house insurance across insurance providers.

To compare your house insurance in minutes, try Quashed.co.nz

How does Quashed.co.nz compare contents insurance

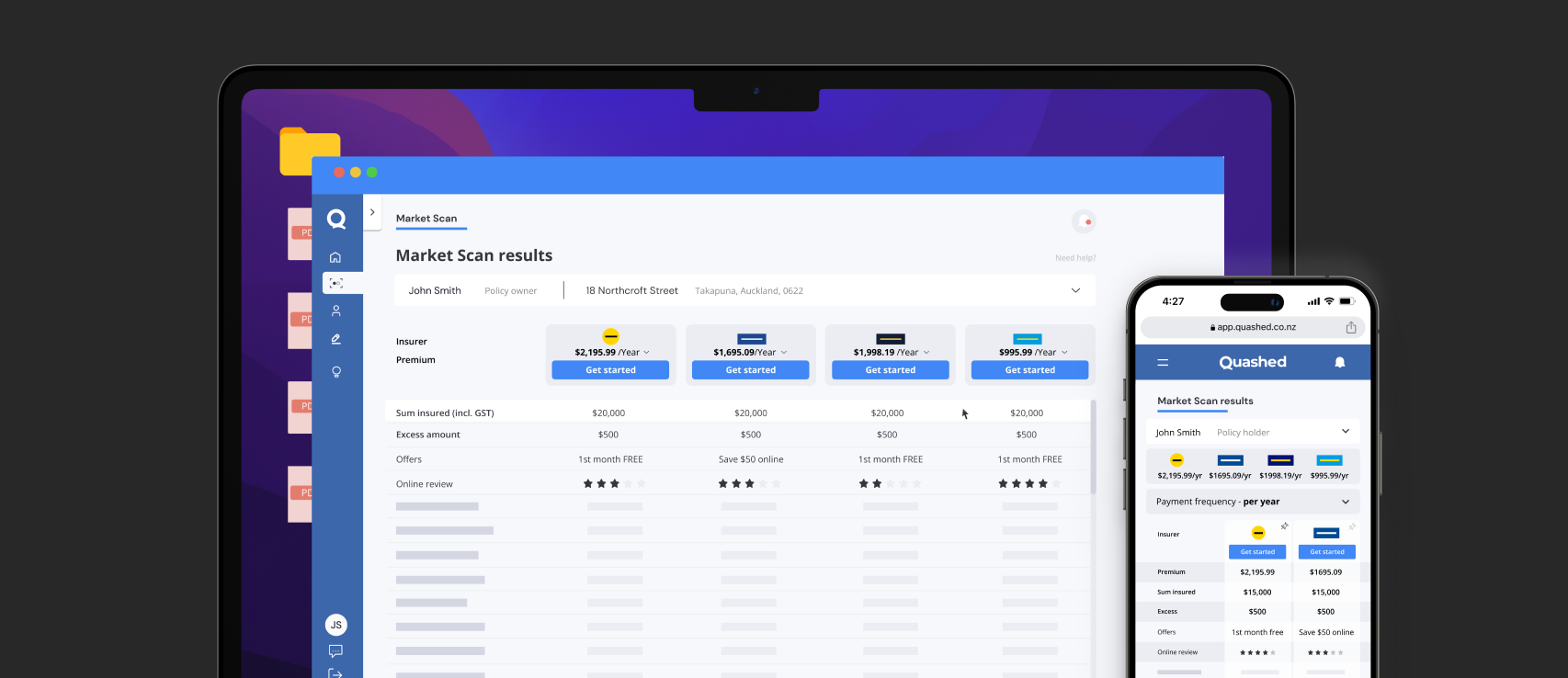

Quashed.co.nz is the first insurance comparison platform of its kind in New Zealand.

It's quick and easy way to compare your contents insurance. Whether you’re shopping for a new house policy, or you’re looking to compare your upcoming contents insurance renewal, Quashed makes it easy.

It takes less than five minutes to shop and compare contents insurance online with Quashed. You’ll be shown real-time pricing across a number of different insurance providers, and you get to see how the policy benefits compare across each insurer shown.

You can choose to upload and compare your existing contents insurance policy against other options, or you can enter your information once and be served up a number of options without having to repeatedly enter the same information on the different insurers websites.

Let’s face it, no one likes shopping for insurance. But Quashed.co.nz makes it quick and easy, some might even say almost fun. Especially when you’re saving hundreds, sometimes thousands, of dollars.

Further reading

Here are some great reads we've selected for you:

Complete Guide to Contents Insurance: Why you need contents insurance and how to find a policy for you

How to Set Your Sum Insured for Contents Insurance: Get it right without breaking your bank account

How To Lower Your Contents Insurance Costs: How to find low cost contents insurance in NZ

How Much Does Contents Insurance Cost: Find out how much contents insurance cost

Average Cost of Car, House & Contents Insurance in NZ: Latest data on car, house & contents insurance in NZ

Contents insurance FAQs

Why should I compare contents insurance regularly

Comparing your contents insurance regularly can help you to save money on your cover when you find a cheaper policy. Contents insurance comparisons also helps you to understand what you can claim on within your contents insurance policy. Insurers often update their pricing, which means their premiums could be cheaper or more expensive.

How can I reduce my contents insurance premium cost

There are several ways to reduce your premiums:

Increase your excess – A higher excess means lower premiums, but also higher out-of-pocket costs when making a claim.

Review your sum insured – Ensure your coverage reflects the true rebuild cost without over-insuring or under-insuring.

Pay your premiums annually instead of monthly – Most insurers charge extra for monthly payments.

Compare quotes with Quashed.co.nz – Shopping your insurance ensures you’re not overpaying. Prices can vary significantly between providers.

Contents insurance basics

What does contents insurance cover in NZ?

Contents insurance can cover damage to your contents and damages to others' property or people (i.e. liability cover). This is the case for both renters and homeowners. Events such as accidents, natural disasters and unexpected events such as vandalism, theft, and more are usually covered if your contents are insured. Coverage varies by policy, but most comprehensive or high tier contents insurance policy will cover:

Natural disaster protection such as flood or fire damages

Accidental damage to your property

Theft of your property

Temporary accommodation and storage costs

Coverage typically includes bicycle, jewellery, phones, tablets, drones, lost or stolen keys, cash etc.

Getting contents insurance cover right

How do I know if I’m insuring my contents for the right amount?

Your sum insured should reflect the cost of replacing all your contents if it was completely destroyed or stolen. If it’s set too low, you may have to cover the shortfall in a claim. Over-insuring can cost you more. You can check out Quashed's contents calculator to understand how much it will roughly costs to replace your valuables.

What should I check when comparing contents insurance policies?

Key factors to compare:

The insurer - Who is the insurer (e.g. their financial rating, where they are based, etc.)

Sum insured – Does the policy fully cover rebuild costs or only the amount you've elected

Policy benefits and limits - What does your insurance cover and how much can you claim

Excess options – A higher excess lowers premiums but increases claim costs.

Policy exclusions – Check what’s not covered, such as gradual wear and tear.

Claims process – Consider customer reviews and insurer reputation.

Additional cover options – Some policies include extras like excess-free cover options

Making a contents insurance claim

What’s the first thing I should do when making a claim?

If an accident occurred, you should check that all parties involve are not hurt. Call for an ambulance immediately if injuries are serious. The police should also be notified.

After which, you should take immediate action to document the damage and notify your insurer.

General contents insurance claims process:

Photograph and video the damage for evidence.

Take down any involved parties' details

Contact your insurer as soon as possible to start the claim.

Prevent further damage if safe to do so, such as covering broken windows.

Keep receipts for emergency repairs or replacements.

Follow your insurer’s process to avoid claim delays.

What happens if I am underinsured for my contents insurance

Underinsurance occurs when your sum insured isn’t enough to cover the full cost of repair or replacement cost of your valuables. If this happens, you will likely have to contribute to the shortfall.

This article provides general information only and does not constitute insurance or financial advice. Insurance policies vary between providers, and you should check with your insurer or a licensed adviser for guidance specific to your situation. For full details, refer to Quashed’s terms and conditions.